Three Key Trends the Manufacturing Industry Faces in 2022, and Beyond

Staying at the forefront of the industries served by Klinger IGI means it’s important for my team and I to stay abreast of the latest trends in aerospace, electronics, and medical/scientific manufacturing.

Thanks to in-person trade shows coming back into play this year, we’ve gained insights from suppliers and customers alike concerning the current state of manufacturing. During the first half of this year, I attended three manufacturing shows: MD&M West, Del Mar Electronics and Manufacturing Show, and Design-2-Part. In addition, our regional sales managers attended the Pacific NW Aerospace Alliance (PNAA) and Inland NW Aerospace Corridor (INWAC) events. These gatherings offered opportunities for one-on-one discussions with industry colleagues who have been facing many of the same industry challenges post-Covid.

Without offering any confidential information, I wanted to share some of the more interesting insights assembled from those interactions. The good news is that what we verified isn’t all bad news. For example, the aerospace market has managed to continue its momentum – though the gains have been at a slightly slower pace than what was earlier forecasted by industry experts. Klinger IGI and our custom parts manufacturing peers have benefitted from commercial aircraft manufacturers taking positive actions to increase their new build and retrofitting activities this year. Yet, moderation in recovery in both of those categories continues, often due to labor shortages. These constraints not only impact the number of aircraft but, more significantly, the underlying cost of production that consumers will ultimately bear. While the horizon for full recovery is a bit more distant than we all anticipated, we’re excited that it is at least commonly perceived to be approaching.

That said, we noted three trends that we expect will continue to present opportunities and challenges in the short term: supply chain shortages, inflation’s broad (and obviously non-transient) effects, and the rising cost and tight availability of labor.

1. Stalled Supply Chains Continue to Impact Manufacturing Across All Sectors

The demand for manufactured goods remains high, burdening already stressed supply chains and further driving shortages of key materials. The automotive industry serves as one of the most visible examples of how a lack of critical materials (such as microchips) can destroy production. The lost inventory backlog that occurred during Covid has been difficult to replace at the demand levels now experienced in the industry. The same can be said of most raw materials.

Chart source: Semiconductor Inventory, compiled by IEEE

Silicone foam and gasket material availability, for example, is the most constrained it has been in a decade. Major silicone producers such as Dow (who now owns Rogers and its high-demand raw materials portfolio) remain extended in their delivery times but are increasing output through various means including overtime and additional capacity. Still, suppliers expect to remain pressured by the shortages into 2023.

Supply chain challenges are not diminishing, but the situation has stabilized at what feels to be something like the low tide point. As a result, we, and the peers with whom we spoke are generally more confident about the reliability of material delivery dates than last year (and even earlier this year). However, we are still seeing those delivery dates run at historical highs. In many cases, the dates remain significantly mismatched to record demand.

While manufacturers can now acquire the key components they need, the long lead times to receive these parts will continue to impact production and encourage different purchasing or inventory tactics at both manufacturer and customer locations. Those tactics are not novel, but they could be uncomfortable depending on the forecasting prowess and financial strength of all players in the chain.

One tactic we all noted to be widely present is higher minimum order quantities (MOQ). Material suppliers – and in turn, material converters, manufacturers, and distributors – are setting MOQ that cover their purchase requirements, with an eye towards gaining financial leverage and lowering the shock of price increases in small volume offers. However, that tactic requires either inventorying or selling greater yields of parts and products. Also, when materials are purchased in higher quantities, other important conditions such as shelf life are increasingly entering into the purchase planning discussions that manufacturers are having with their customers.

Another tactic in increased use is materials substitution. Customers who limit themselves to a single material source specification for their product are the ones experiencing the most severe impacts from the persistent supply line delays and price hikes. Conversely, customers who preapproved alternate materials that are functional equivalents – or those who are now willing to unlock their exclusivity specification to keep their lines running – are experiencing a less pronounced bite to their financials than those who stood their ground awaiting a proprietary material’s delivery. Here’s why. Those customers were getting materials earlier, and sometimes at a more favorable cost. As a result, build-to-print parts manufacturers are experiencing that their customers are more agreeable to becoming ‘material agnostic’ than they were if that’s the only choice to keep their lines running.

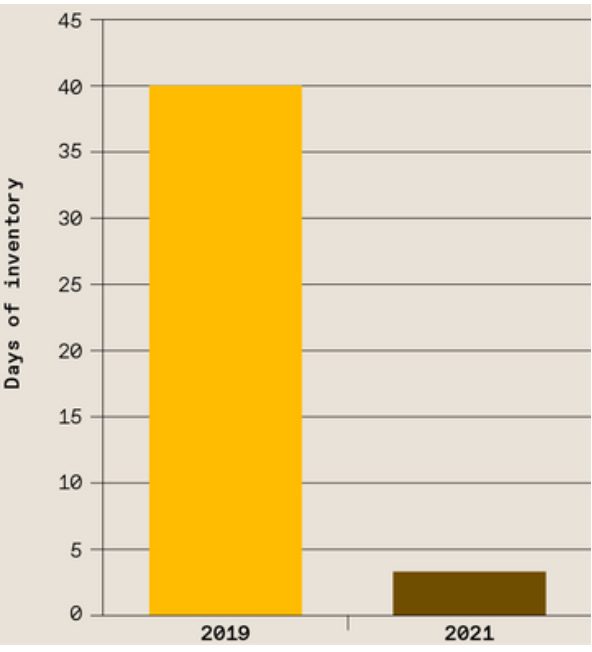

Additionally, many customers have executed blanket purchase agreements to secure a place in line for materials and parts. This tactic has been especially important for highly engineered materials that tend to move in and out of allocation when demand spikes. This obviously increases pressure on customers to forecast to extended timelines. Such long-range forecasting can be risky because it depends on the reliability of sources for a product’s demand information. Yet, more companies are doing this than pre-Covid. We have noted (and data confirms) that inventory levels are running at higher than historical rates to assure there is a continuous flow in and out of the warehouses.

Chart Source: US Census Bureau US Business Inventories data compiled by TradingEconomics.com

When judging what is worse, most manufacturers prefer to have materials in the pipeline and maintain higher inventory costs than risk allowing the pipeline to dry out and restart later when demand could be even higher and supplies even lower. This tactic obviously favors well-capitalized companies.

With the time to acquire key raw materials often running between 16 to 32 weeks, it’s important that the above tactics are recognized and used as effective counters to the persistent supply chain frustrations affecting the manufacture of critical aerospace, electronics, and defense parts.

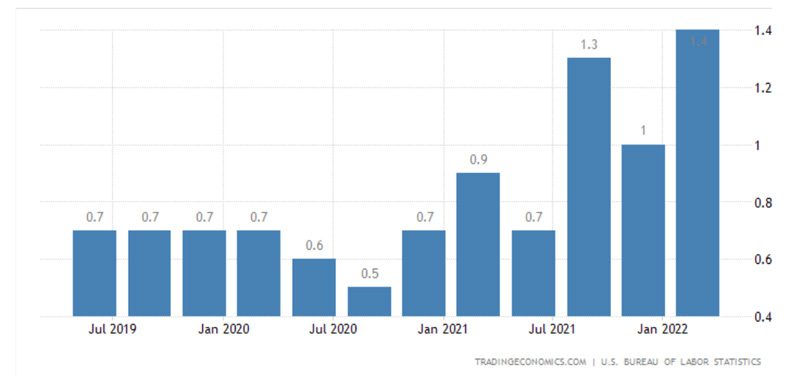

2. Inflation’s Impact Continues to Ripple Across All Industries

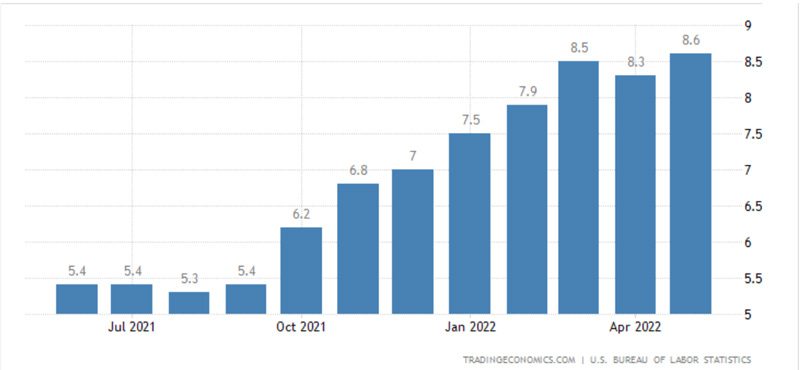

Inflation is not the transient event that government leadership represented in 2021. And it’s not something that any supplier or manufacturer can afford to accept passively by absorbing it into their cost of operations. Higher costs of operation must be passed through the supply chain. That trend has invariably resulted in rising wholesale and end-user prices. With inflation the highest it has been in four decades, we can expect to see historically elevated prices in materials and finished goods, with more increases keeping in lockstep with inflation as it embeds itself firmly into supplier manufacturing costs.

Chart Source: US Bureau of Labor Statistics US Inflation Rate data compiled by TradingEconomics.com

Inflation has become the most significant factor to almost every aspect of manufacturing operations – wages, insurances, facilities, utilities, travel, and much more, beyond the already notable leaps in material cost. Further, inflation is now perceived to be structural in the commerce of the goods and services we and our industry peers deliver. It is driving what we and our peers feel could be an irreversible condition to the formulation and fulfillment of future sales offers.

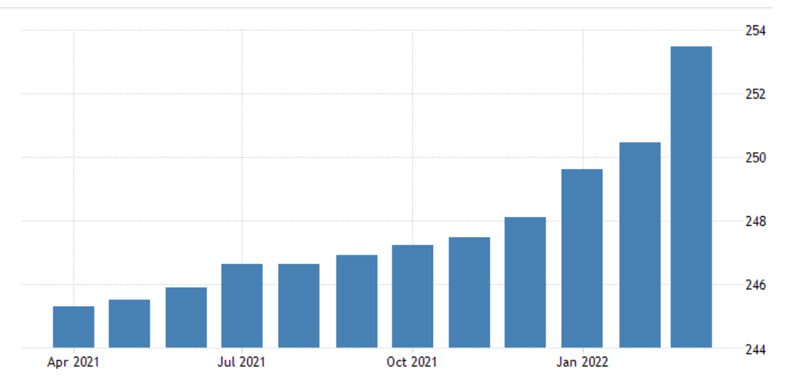

With price hikes for materials continuing to be significantly higher than their respective price index’s growth, expectations for soft increases have all but disappeared. Consider aerospace parts manufacturing data and pricing trends. The price changes on many commonly used engineered materials used in a custom part’s manufacture have exceeded 20% year over year, creating a force majeure condition in some instances for some manufacturers. Compounding that, as energy costs continue to increase, freight costs on inbound (to the fabricator) raw materials and outbound (to the customer) finished goods continues to grow. That said, passing on higher prices at distinctly higher year over year rates is the only way manufacturers can meet their financial obligations. It is an untenable financial proposition to hold to cost escalation parameters developed years ago when inflation was 3% or less.

Chart Source: US Federal Reserve US Producer Price Index (Aerospace Product and Parts Manufacturing) data compiled by TradingEconomics.com

3. The Rising Cost and Tight Supply of Labor

A tight labor market has led to an expected increase in labor costs. Year over year increases to wages and benefits are roughly double what they were in 2020. Referencing the same JP Morgan business outlook survey, 70% of the respondents said that recruitment and retention constituted their second largest concern behind inflation. We concur with their view of its potency.

Chart Source: US Bureau of Labor Statistics Employment Cost Index QoQ data compiled by TradingEconomics.com

A poor labor market is a trend that will continue to impact both the delivery and pricing of products. Manufacturers have found it increasingly difficult to fill open positions caused by attrition or retirement. Plus, new entry level hires expect wages above prior industry averages, provoking adjustment of current employee wages to maintain a fair workplace. All of this impacts a manufacturer’s operating costs, and the differential is embedded into price offers with greater boldness and regularity.

Chart Source: US Bureau of Labor Statistics US Nonfarm Unit Labor Cost data compiled by TradingEconomics.com

The consensus of our discussions with our industry counterparts was this: If you can land a good worker, keep that person at all costs. As a result, and in conjunction with more periodic wage adjustments, we’re seeing trends in employer-paid benefits that to date have been either not offered or which were thinly subsidized. Like it or not, the employer no longer possesses the advantage in the bargain for what an employee will deem acceptable when there are often many other openings in their industry for their skill set. Thus, maintaining competitive wage and benefit programs is more of an expectation than a discriminator today. That means work culture, flexible work arrangements, and various incentives are proving to be more influential to employee satisfaction and retention than previously considered by many employers. Those all come at a cost – and again, that cost will find its way into the supply chain, and into the hands of the customer.

What’s Ahead of Us

The JP Morgan Business Leaders Outlook Pulse surveys 1,500 business leaders of companies with $20 to $500 million in annual turnover. The 2022 survey was recently published. In it, only 19% of the business leaders surveyed were optimistic about the economy for the year ahead. (In the 12 years of the report’s publication, this was the lowest survey result ever.) This compared to the 2021 survey data that returned an expression of 75% optimism for 2022. So, “Sit down, strap in, and hold on.” Both the earlier shown data and this noteworthy industry leadership sentiment suggest the things both challenging us in the manufacturing business and disturbing us about costs are neither trending nor perceived to be leveling out soon.

While not suggesting we’ve experienced an inflation-driven shift to a seller’s market, it is evident that we are now in a market that encourages new buying tactics for managing delivery, inventory, and cost. Those tactics must increasingly accommodate their supplier’s (and their raw material sources’) capabilities and financial impacts. Else, there will be a loss of suppliers and the resulting loss of supply – and nobody needs self-inflicted disruptions when the market is already doing more than its fair share to trip everyone up.

The tactics earlier mentioned may address some ways to mitigate the challenges. However, they are only a few of many possible ones – and they may not be appropriate to your industry, customer base, or organization’s financial structure. Nonetheless, they are options to consider.

So, make sure you’ve got a strong manufacturing partner who can advise best material purchasing and order fulfillment strategies – with the goal to help you maintain reasonable levels of inventory and product in the pipeline to avoid another supply-driven hard stop and restart. Again, the supply chain is doing better, but it is still fragile. And demand is mercurial – so what was available once before may not be later at the same delivery and price. In this environment, more realistic goals are reliable (vs. rapid) delivery and cost control (vs. cost reduction). In short, it’s broadly considered among those with whom we spoke that it is more important to get parts and products through production to the customer, and to try different ways to limit the magnitude of price elevations as all costs of manufacture grow remarkably now (and if the US business leaders perceive correctly, into next year). To that end, we hope these insights have been helpful.